What you need to know about a reverse mortgage

Ron Bush

50plus Magazine

Most have heard about reverse mortgages, but few have a real understanding of how they can be used as a financial strategy. Following is a brief overview of the benefits and FAQs about RM.

First, let’s bust this myth about RMs: the bank does not own your home. It holds the mortgage; you own your home.

A Reverse Mortgage (RM) is a Home Equity loan, like those offered by banks and credit unions, but more flexible and administered by the FHA. The official name is Home Equity Conversion Mortgage (HECM).

Many think of a RM as a Last Resort — “we’re out of money but have the house. Shall we sell it or get a RM?” Today, financial planners integrate RMs with a family’s total financial resources to achieve maximum benefit, such as to strengthen Social Security payments, other investments, or both.

A RM has many benefits other loans lack. Following are just a few:

- Allow you to continue living in your current home

- Use an RM to “double your buying power” in a new home

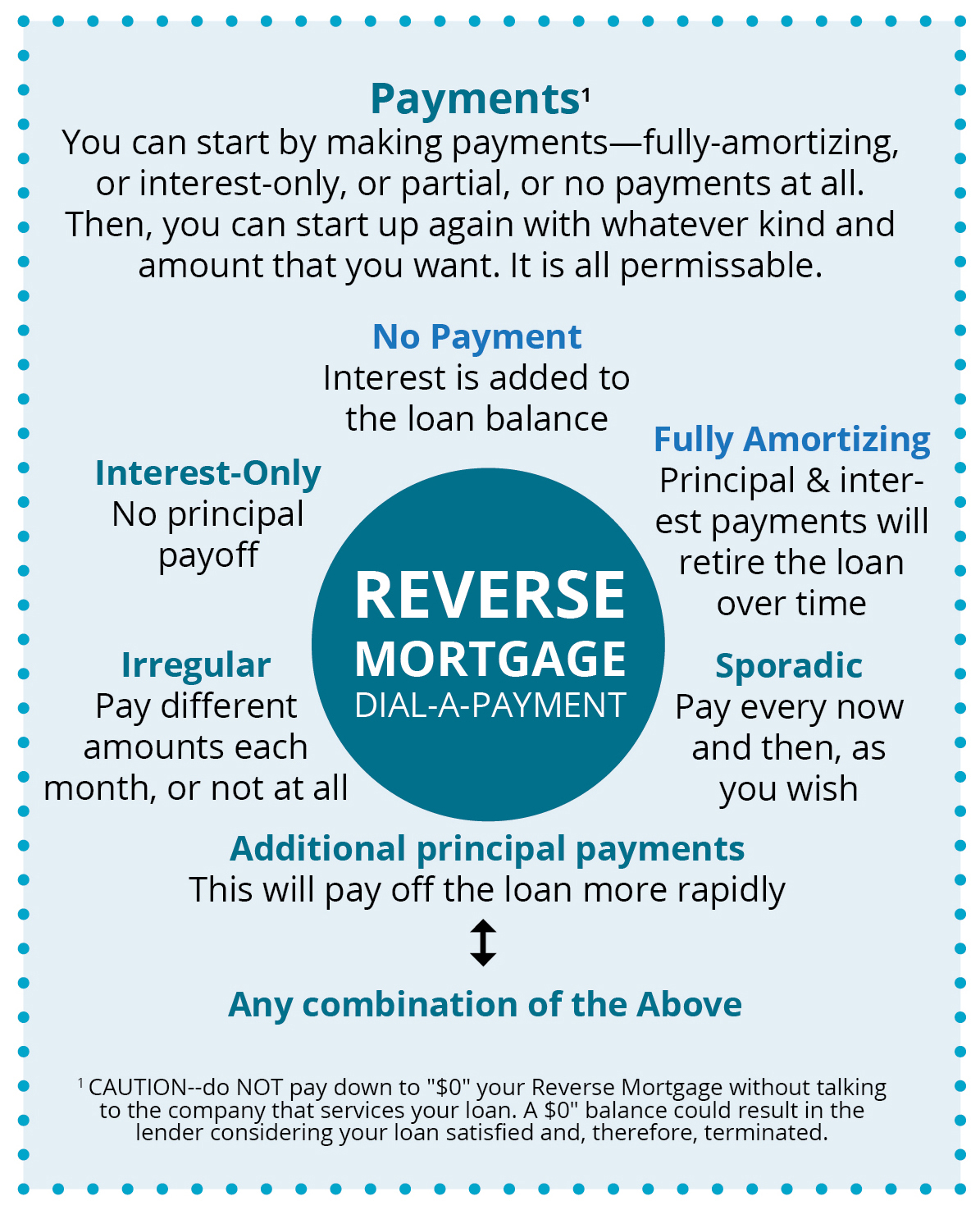

- Make no payments ever (even if the loan balance grows larger than your home is worth)

- Make any combination of payments (principal & interest, interest-only) or no payments at all

- Make payments on the loan principal and then reborrow repeatedly without starting a new loan

- Receive all available equity at one time, in a lump sum or in monthly payments for life while occupying your home, even if they total more than the home’s value

- Use the RM as a line of credit that is always growing (called “Principal Limit Growth”)

- Receive higher Social Security payments by delaying benefits

- Allow your investment portfolio to grow before tapping into it

- Not be personally liable for the RM loan

The following are answers to frequently asked questions:

- When is the RM loan due?

A: When you no longer reside in the home.

- Can I pay down the balance of my RM?

- Yes. But do NOT pay off the loan as it will be closed, nullifying any remaining benefits.

- Who gets the home when I’m gone?

A: Your heirs.

- I’ve heard the bank takes it away from the family?

A: Only if the bank must foreclose.

- What happens if the loan balance is more than the home is worth?

A: Your heirs are not liable for the loan. The lender is paid by FHA mortgage insurance.

- What if my family wants to keep the house but the loan balance is more than the home value?

A: Heirs can pay the lender 95% of the appraised value; the lender then forgives any remaining balance.

- What if the loan balance is more than the home’s value andthe family does not want the home?

A: The family deeds the property to the lender, or the lender forecloses. No one is personally obligated.

- If the loan balance is less than the home’s value, who owns this equity?

A: Your heirs.

- Can I qualify for a RM at my age and income?

- Yes. If you are 62, your FICO score is not as important as a history of paying your bills and sufficient income to pay taxes, insurance, HOA fees and home maintenance.

- How much can I get from a RM?

- It is based on age, the appraised home value and interest rate. Today’s low-interest rates allow you to get more equity in your RM.

This article is a simple primer, for informational purposes only. To learn more about the features and benefits of RM loans, consult a qualified professional.

Ronald Bush is a Licensed Real Estate Broker in Oregon, and retired Attorney. Reach him at Equinox Real Estate 541-514-1141.